If an arithmetic error was made when calculating wages, as a result of which the employee received a larger amount, he must return the difference. The employee can return the money himself or write a statement requesting that the employer himself withhold the amount from the next salary.

The employee returns the money himself

An employee can deposit money at the organization's cash desk (Debit 50 Credit) or transfer it to a current account (Debit Credit).

If an employee was credited with one amount and paid a larger amount, then everything will fall into place in terms of turnover when the employee makes up for this difference.

In the case where the error was precisely in the arithmetic calculation of wages in accrual, the following entries need to be made:

- Debit 20 ( , …) Credit – reverse excess payroll

- Debit 73 Credit - write off the excess amount for other settlements with employees

After the amounts for wages have been corrected, do not forget to eliminate the erroneous amounts for both personal income tax (reversing the tax accrual for debit and credit 68 personal income tax), and for insurance premiums (reversing entry for account 20 (, 25...) and credit 69 accounts)

The organization erroneously calculated and paid (minus income tax) a salary of 30,000 rubles to an employee. for May, instead of 000 rubles. The employee returned the money to the cashier.

Postings:

| Account Dt | Kt account | Wiring description | Transaction amount | A document base |

| Employee salary accrued | 30 000 | |||

| 68 personal income tax | Personal income tax withheld | 3900 | Payroll statement | |

| 50 | Salary paid for May | 100 | Account cash warrant | |

| The amount of the salary surplus has been reversed | — 2000 | Payroll statement | ||

| 68 personal income tax | Personal income tax reversed | -260 | Payroll statement | |

| 73 | The excess amount was transferred to other settlements with the employee | 1740 | Payroll statement | |

| 50 | 73 | The employee returned the money to the cash register | 1740 | Receipt cash order |

Employer withholds money

Upon application to the employee, the employer may withhold the overpaid salary himself. To do this, make notes:

- Debit Credit 73 – overpaid amount is withheld from salary

In the month of erroneous accrual, reversing entries are made for the calculation of salaries, taxes and contributions.

The employee wrote an application to deduct from his salary for June (accrued 24,780 rubles) the overpaid amount of 3,500 rubles. for May.

Postings:

| Account Dt | Kt account | Wiring description | Transaction amount | A document base |

Subject: “Features of calculation, payment and deduction of wages”

Duration: 7 o'clock

Price: 8900 rubles

Organizing company:

School "SKB Kontur"

tel. (495) 660-06-17,

school.kontur.ru

Is the employee obliged to return the overpayment?

All situations where money overpaid to an employee can easily be withheld from the salary at the initiative of the company are listed in Article 137 of the Labor Code of the Russian Federation. I will name the most common ones.

First of all, you have the right to withhold from the employee the money previously given to him, which he did not return or did not work out. For example, he did not report on the money received for household needs or did not submit an advance report after returning from a business trip. In addition, if an employee resigns, the unearned salary advance, as well as excess vacation pay, can be withheld from him. However, in some cases, unearned vacation pay cannot be withheld. Let's say in case of reduction.

Another situation is that an employee was overpaid due to his illegal actions, which was confirmed by a court decision. For example, when applying for a job, he presented you with a fake higher education diploma.

And finally, the most common situation, which we will consider in detail, is that an employee was paid more money due to an accountant’s error or a glitch in a computer program. Here I will immediately make a reservation: the company has the right to withhold an overpayment only if there is a counting error. The same procedure applies to vacation pay.

CALCULATE SALARY

The electronic service “Payroll Calculator” will help you check and clarify the amount of benefits. Moreover, with its help you can easily calculate the amounts of vacation pay, travel allowances, bonuses, etc.However, not a single regulatory document says what a counting error is. In practice, this is considered to be any inaccuracy made in arithmetic calculations. For example, an accountant added or multiplied numbers incorrectly. And if you used the wrong algorithm for calculating vacation pay or, say, took into account extra payments, such an error is no longer countable. Now let’s imagine this situation: an employee’s salary was transferred twice during the same period. So, such an error does not apply to accounting, since the salary was calculated correctly (ruling of the Supreme Court of the Russian Federation of January 20, 2012 No. 59-B11-17). Likewise, if the order specifies one employee, and the payment is accrued, for example, to his namesake, the company will not be able to claim the funds received.

Of course, the employee can reimburse any overpayment at his own request. Employees usually do this to avoid conflict with their employer. If the employee has already spent the money, you can agree with him that the company will gradually withhold the overpayment from him.

At the same time, do not forget that the total amount of all deductions for each payment of wages cannot exceed 20 percent, and only in exceptional cases - 50 percent (Article 138 of the Labor Code of the Russian Federation).

At the same time, the employee himself can dispose of his salary as he wants. To do this, just write an application to the company’s accounting department. The provisions of Article 138 of the Labor Code of the Russian Federation do not apply here. That is, in this case you can hold on to anything and for as long as you want. Representatives of Rostrud emphasized this in a letter dated September 16, 2012 No. PR/7156-6-1.

PARTICIPANT QUESTION

– Instead of sick leave, the employee was given a salary. How to fix this error?

– First of all, recalculate. Namely, instead of salary, calculate benefits for those days when the employee was sick.

If it suddenly turns out that the amount of sick leave is more than the salary for these days, simply pay the employee the difference. But the opposite situation is much more likely. That is, you gave the employee more than he was supposed to. In this case, offset the excess amount against future accruals. But only with the written consent of the employee himself.

The situation is more complicated if the employee has already left the company. After all, the employer has the right to withhold funds only from employee salaries. Here it turns out that there is nothing left to hold on to. The employee quit, which means he will no longer receive a salary from the organization.

In this case, the employer has only one way to recover the extra money - going to court. Of course, if the employee does not agree to return the overpayment voluntarily, and the organization has the right, according to labor legislation, to demand a refund.

For example, if we are talking about overpaid vacation pay, the debt will have to be forgiven. The fact is that the court will be on the side of the employees. And it doesn’t matter that today the legislative norm that previously prohibited employers from collecting unearned vacation pay in court has lost force (paragraph 3, paragraph 2 of the Rules approved by the People’s Commissar of the USSR on April 30, 1930, No. 169).

In any case, the resulting holiday pay debt cannot be considered unjust enrichment. After all, this can only be discussed in case of dishonesty on the part of the employee or a counting error (clause 3 of Article 1109 of the Civil Code of the Russian Federation). Here are examples of cases decided in favor of workers - rulings of the Moscow Regional Court dated December 15, 2011 in case No. 33-25971 and the Moscow City Court dated August 8, 2011 in case No. 33-23166.

How to reflect an overpayment in accounting

All accounting corrections must be made in the period in which the error was identified. To do this, simply reverse the overcharged amount. Also reverse the personal income tax amount. After all, the employee must return to you only the amount that you transferred to him. The postings will be like this:

DEBIT 20 (23, 25, 26, 29, 44 ...) CREDIT 70

– the excessively accrued amount of wages is reversed;

DEBIT 70 CREDIT 68 subaccount “Settlements with the budget for personal income tax”

– the amount of excessively withheld personal income tax was reversed;

DEBIT 50 CREDIT 70

– the overpayment is returned to the cash desk (if the employee has chosen this method of repaying the debt).

And if an employee asks to withhold extra money from his salary, the first two entries are sufficient. In this case, it is not necessary to reverse the contribution entries. Just when you calculate them at the end of the month, do not forget to subtract the amount of overpayment from the base.

What documents need to be completed

The basis for correcting documents and recalculating will be an internal memorandum (see sample below. – Editor’s note). Describe in it what mistake was made and what needs to be done to correct it.

Next, inform the employee himself about the overpayment (see sample notification below. – Editor’s note). In this letter, indicate the amount you are asking to be returned, and also state the reason why the employee received the extra money. Please familiarize the employee with the letter and sign it.

ABOUT THE LECTURER

Vyacheslav Vladimirovich Shinkarev graduated from the Ural State University named after. A. M. Gorky, Faculty of Mathematics and Mechanics, majoring in mathematics. And from 1996 to the present time he has been working at the company ZAO PF SKB Kontur. He currently holds the position of head of the development group for the Kontur-Salary program. At the same time, he works as a consultant on the Accounting Online portal.

If the employee does not agree to pay cash, but does not object to the overpayment being deducted from the salary, the manager issues an order to withhold (see sample below. - Ed. note). The employee must sign the order, indicating that he does not object to the basis and amount of deductions (letter of Rostrud dated August 9, 2007 No. 3044-6-0).

Moreover, written confirmation is necessary even if the company has the legal right to withhold overpayment from the employee.

At the same time, you have the right to withhold money, including from the advance payment of wages for the first half of the month. And it’s better to do just that. The fact is that when calculating deductions only once at the end of the month, you may be faced with the fact that the employee’s salary minus personal income tax and the advance payment already paid may not be enough to recover the entire amount. Or the second part of the payment will be significantly less than the first. After all, there is no need to withhold personal income tax from the salary advance.

PARTICIPANT QUESTION

– Will I have to recalculate taxes and contributions?

– In our case, we are talking about overpayment to an employee who continues to work in your company. This means that you just need to reduce the current accruals in favor of this employee by its amount. This rule applies to income tax, contributions to funds, and personal income tax. The fact is that there is no error in the calculation of the base. This means that there is no need to clarify reports for previous periods.

Abstract prepared by Sergey Shilkin

Star

for the correct answer

Wrong

Right!

The company paid the employee more vacation pay than he was entitled to. The error is not an accounting error, but the employee agrees to have the excess withheld from his salary. Is it necessary to apply the 20 percent limit in this case:

The employee has the right to dispose of his salary at his own discretion. If he writes a statement to the company’s accounting department, more than 20 percent can be withheld from him. will bring a duplicate of the sick leave certificate with the correct information.

The employee must confirm his consent to withholding the overpayment in writing.

If the employee does not promptly return the balance of unused funds to the cashier, Art. 137 of the Labor Code, which provides for cases of deduction from an employee’s salary to repay his debt to the employer.

The employer makes and formalizes decisions, as a rule, in the form of an order or instruction, although a unified form of such an order is not established by regulatory legal acts.

With regard to the employee’s consent to withhold amounts from wages, his written consent should be obtained.

As a general rule, deduction of overpaid amounts from wages is prohibited. But still, it is carried out in a limited list of cases directly provided for by the Labor Code of the Russian Federation. Let's consider how and under what circumstances it is possible to return the amount given to an employee in excess.

When does an employer have the right to withhold overpayments?

According to Part 2 of Art. 137 of the Labor Code of the Russian Federation, the employer has the right to deduct debt from an employee’s salary:

- if the employee for some reason has not worked out the prepayment received;

- in order to reimburse the unspent part of the prepayment for a business trip, moving to another area, etc.;

- in case of correction of errors made by the accounting department in wage calculations;

- to reimburse the payment received by an employee guilty of failure to comply with labor standards or idle time;

- upon dismissal in order to reimburse vacation pay for the unworked period of previously received vacation.

In all of the above cases (except for the first), the employer has 1 month to make a decision on deductions from wages.

As a general rule (Part 4 of Article 137 of the Labor Code of the Russian Federation), deduction of overpaid wages is not allowed. However, there are some exceptions. Let's look at them.

Refund due to inaccuracy in calculations

To withhold overpaid wages on this basis, it is important to understand that wages mean remuneration for work, since the above prohibition does not apply to other payments.

Information on how to distinguish payments included in wages from other types of remuneration can be found in the article .

Inaccuracy in calculations is grounds for the return of overpaid wages if the person who calculated it made an error. For example, when adding the amounts of bonus (200 rubles) and salary (10,000 rubles), instead of 200, 2,000 was entered into the calculation (i.e., an extra zero was indicated), etc.

Recalculation if there is guilt in non-compliance with established labor standards or simple

To apply this basis, it is important to know:

- what is non-compliance with labor standards (Article 155 of the Labor Code of the Russian Federation);

- what is meant by downtime (part 3 of article 72.2 of the Labor Code of the Russian Federation).

According to Art. 160 of the Labor Code of the Russian Federation, labor standards mean various (temporary, quantitative, etc.) standards provided for by a given employer.

From Part 3 of Art. 155 of the Labor Code of the Russian Federation follows: if an employee has not met the standard due to his own fault, he is paid a part of the salary corresponding to the fulfilled part of the standard.

According to Part 3 of Art. 72.2 of the Labor Code of the Russian Federation, downtime is understood as a temporary cessation of work for various reasons.

Based on Part 3 of Art. 157 of the Labor Code of the Russian Federation, the employee’s guilt during downtime is a reason for the employer not to pay him.

Examples when an employee is guilty of downtime:

- got into an accident, violating traffic rules;

- refused training in occupational safety rules and was suspended from work.

Such cases may lead to salary recalculation.

Committing illegal actions that resulted in excessive payment

This is one of the most difficult grounds for an employer, since the legislation does not contain specific criteria for unlawful actions. Consequently, any illegal acts that result in receiving a salary in a larger amount than required can be recognized as such. The illegality must be confirmed in court. Therefore, in order to use this basis, the employer must have appropriate evidence.

For example, if an employee falsified documents confirming the fact of his employment, the employer will have the right to demand the return of unlawfully received wages.

In each specific case, the relevant criteria for the illegality of an employee’s actions are subject to consideration by the court, taking into account all the circumstances of the case.

How to return overpaid wages?

In order to correctly process the withholding, the employer should:

- Issue an administrative act (for example, an order) on behalf of management on the deduction of appropriate amounts from the employee’s salary, indicating in it the grounds and general amounts of such deduction.

- Familiarize the employee with this act against receipt.

- For each salary payment, hand over to the employee a payslip indicating the grounds and specific amounts of deduction from this payment (Article 136 of the Labor Code of the Russian Federation).

In order not to violate the employee’s right to payment when deducting from wages, it is necessary to take into account the restrictions established by Art. 138 Labor Code of the Russian Federation.

The amount of deductions is determined from the amount remaining after deducting personal income tax.

The deduction limits are as follows:

- as a general rule, the maximum amount of all deductions is no more than 20 percent (at the initiative of the employer and in the absence of objections from the employee);

- in cases reflected in federal laws, 50 percent may be withheld;

- in some cases provided for in Part 3 of Art. 138 of the Labor Code of the Russian Federation (collection of alimony, compensation for harm, etc.), the withholding can be 70 percent.

The last 2 points are applied by court decision or as a result of enforcement proceedings.

Situations are possible when an employee independently expresses a desire to have more deducted from his earnings than is limited by law. In this case, he will be required to submit an application addressed to the employer.

Results

Deduction of overpaid amounts from wages is prohibited, except for a number of reasons. The relevant grounds are listed in Part 4 of Art. 137 Labor Code of the Russian Federation. When withholding, it is necessary to comply with the restrictions established by Art. 138 Labor Code of the Russian Federation.

14.12.2018

Sometimes when paying for labor, an accountant may make a mistake and underpay or overpay the salary.

In the first case, you can always make an additional payment.

But the overpaid amount can only be recovered in a limited amount.

The law also introduces restrictions on the possibility of deduction depending on the reason for which the overpayment was made.

What to do if an employee is overpaid?

In practice, overpayment of wages can be made for a number of reasons.

If the accountant allowed it, there are three options for getting out of the situation:

- Talk to the employee and ask voluntarily contribute excess amount paid to the company's cash desk. This method is especially rational when the payment has just been made and the money has not yet been spent.

- Commit retention overpaid amount in writing. You can set certain amounts of deductions for a specified period, but not more than 20% of the monthly salary.

- Submit a claim to the court for the purpose of forced recovery of the excessively overpaid amount. This option is used if the employee does not want to return the excess amounts and has not written consent to the deduction.

A copy of the document is sent to the employee for review. After that an employee deposits an excess amount into the company's cash register, agrees to the withholding, or the employer files a lawsuit.

Read also:

Is it possible to deduct the amount of overpayment from the employee’s salary?

The legislator is quite strict regarding the issue of collecting amounts overpaid to the employee.

Art. 137 of the Labor Code of the Russian Federation contains a list of cases of overpayment when it is allowed withholding overpaid money:

Art. 137 of the Labor Code of the Russian Federation contains a list of cases of overpayment when it is allowed withholding overpaid money:

- when reimbursing an unpaid advance;

- return of unspent travel allowances;

- when making calculation errors;

- in case of overpaid vacation pay (except for the cases of clauses 1 and 2 of Article 77 and clauses 1, 2, 5, 6,7 of Article 83 of the Labor Code of the Russian Federation);

- the overpayment was made due to unlawful actions of the employee recognized by the court;

- if the labor authority has proven a violation of the norms.

Under other circumstances, the employer will not be able to recover the excessively overpaid amount from the employee’s salary.

In the Labor Code of the Russian Federation it is impossible to find a specific concept of a counting error. But, according to letter No. 1286-6-1 dated October 1, 2012, an error made as a result of arithmetic calculations is recognized as a counting error.

Let's give specific examples in table form:

In practice, most situations are resolved peacefully. An employee who has received an undue amount independently deposits the overpaid money into the company's cash desk or agrees to have it deducted from wages.

How much can a penalty be collected?

Art. 138 of the Labor Code of the Russian Federation establishes a limit on the amount of deductions from wages in the amount of 20%. Therefore, the period of debt collection may drag on for several months, depending on the amount of debt.

Example:

Suppose an employee was overpaid by 10 thousand rubles.

Suppose an employee was overpaid by 10 thousand rubles.

His monthly income is 20 thousand rubles.

20% of 20 thousand is 4 thousand.

According to the law, it is impossible to recover more than this amount from an employee even with his consent.

Therefore, with such a salary, the entire debt will be collected with deductions for 3 months (4000 + 4000 + 2000).

By agreement of the parties It is also possible to set a smaller deduction amount from wages.

For example, an employee and an employer came to an agreement on monthly deductions from salary in the amount of 10% to repay the debt that arose due to overpayment as a result of an accounting error by an accountant.

If an employee wants to repay the debt in large payments, he can simply receive a salary and then pay the debt yourself in an amount exceeding the statutory 20%.

How to apply correctly?

To legally record a billing error and overpayment, it is recommended draw up a special act. It is compiled in 2 copies.

The document is signed by each member of the commission; its composition can include: an accountant, chief accountant and other persons of the enterprise.

One copy of the document remains in the organization, the second, along with the notice, must be given to the employee against signature.

The notice specifies the amount of overpayment, the need to repay it and the deadline.

If an employee refuses to pay a debt or remains silent in response to a notice, collect the debt from wages the employer has the right only through a judicial authority.

Letter No. 3044-6-0 of Rostrud dated 08/09/2007 states that the employee’s consent to withhold excessively overpaid amounts from wages must be drawn up in writing.

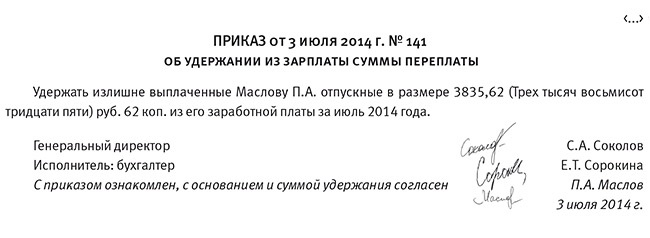

Within a month the employer issues debts from wages.

It contains information:

- setting the task for the accountant to withhold the amount of debt from the employee’s salary;

- employee personal data;

- amount of deductions;

- from what month the funds will be withheld;

- grounds;

- manager's signature;

- date of.

The employee must be familiarized with the order and signed.

Only after such manipulations have been completed the employer has the right to withhold excess amounts.

If necessary, resign between the employee and the employer an agreement is concluded on the timing and amount of debt repayment on a voluntary basis.

If the debtor does not make the required payments, the employer will use this document has the right to go to court with permission to collect through bailiffs.

If an employee quits, and after that the employer discovers that he has overpaid the amount to the employee, then the organization writes notice demanding payment of debt, otherwise an appeal to the court will follow.

When going to court a statement of claim is drawn up and a package of documents is attached to it:

- employment contract with the employee;

- documents on calculation and payment of wages;

- report on the identified error;

- notification, with confirmation of delivery to the dismissed employee.

If part of the debt has already been paid, additional attach a certificate with the balance of the debt at the time of going to court.

At the end of the trial, the court issues an order to collect the debt or refuse to satisfy the claim.

If the decision is positive, then the resolution is sent to the bailiffs to open enforcement proceedings and collection of the amount owed.

conclusions

On the topic of recovering overpaid amounts from wages, several main conclusions can be drawn:

- Withholding can be made in an amount of no more than 20% per month from wages.

- The employer must obtain the employee’s consent and issue an appropriate order to the enterprise.

- If the employer refuses to pay the debt, the employer has the right to go to court to resolve the issue.

- Art. 137 of the Labor Code of the Russian Federation establishes certain situations regarding overpayments in which deductions from wages and collection of the amount of debt through the court are allowed.

Payroll calculation is a labor-intensive and painstaking procedure. Despite the widespread automation of this process, an accountant is not immune from errors. Failures in the operation of computer equipment also occur, which can result in incorrect calculations and overpayment of wages to employees.

Having discovered an error, the accountant often makes an automatic deduction from the next month's accruals based on settlements with the employee, making the appropriate entries in accounting. Is such a “simple” way out of the situation legal? In what cases does an organization have no right to withhold excess wages paid? Is an accountant responsible for errors in payroll calculations? Let's find out in the article.

Returns are not always possible

It should be said right away that “automatic” deductions of amounts overpaid to an employee from the next month’s wages or failure to issue part of the wages in cash from the cash register under the same conditions are illegal.

Resolving an unpleasant situation for an accountant should begin with receiving a statement from the employee, in which he asks to withhold the excess amount of money received or undertakes to pay it in cash voluntarily.

It is possible to do without written consent only in some cases described in the Labor Code of the Russian Federation (Article 137):

- the presence of a counting error, i.e. such an error that can be attributed to arithmetic;

- the calculation was made on the basis of false information received from the employee (for example, false documents for deductions);

- the calculation was made on the basis of false information from the primary documents for calculating wages (for example, according to the documents, the production output standard was met, but in fact it was not).

As a rule, such situations, in particular, the submission by an employee of false information that affects the calculation of “salary” amounts, are resolved in court (see the Labor Code of the Russian Federation, the same article).

If the employee has expressed in writing his consent to repay the overpayment, the employer can withhold it only for a month after the end of the period specified for the return of advances, debts, and incorrectly accrued amounts of payments.

Counting error and judicial practice

The presence of a counting (arithmetic) error is the most common argument of the employer when withholding overpaid amounts of wages. However, judicial practice in this area most often does not work in favor of organizations.

Example: The Moscow Regional Court, in its ruling No. 33-19764 dated 10/12/10, expressed the opinion that the overpayment cannot be a calculation error, but is a consequence of the employer’s incorrect application of labor legislation. According to the judges, the overpayment cannot be attributed to the amounts of unjust enrichment (Civil Code of the Russian Federation, Art. 1109). The employee is not obliged to return the funds overpaid to him. In addition, not all courts recognize a malfunction in an accounting program as a counting error.

Example: The Sverdlovsk Regional Court, in its ruling in case No. 33-7642/2016 dated 04/21/16, did not recognize a technical counting error, but the Samara Regional Court in its ruling No. 33-302/2012 dated 01/18/12 did.

Judicial practice on the application of Art. 137 of the Labor Code clearly indicates that the following cannot be recognized as a counting error:

- payment for a longer vacation than the employee is entitled to by law;

- payment of a larger bonus;

- erroneous payment of double wages for the period.

This is evidenced by numerous decisions of courts of all levels, up to and including the Supreme Court (definition No. 59-B11-17 of 01/20/12).

On a note! Rostrud, in its letter No. 3044-6-0 dated 09-08-07, expresses the point of view that even if there is an undeniable accounting error, the employee’s written consent is required to repay the difference at his expense.

Documentation of the return of excess payments

Having discovered an error, the accountant is obliged to report it to the management of the company. Next, an act is drawn up, which records the fact of overpayment, amount, accrual period and other essential information. Members of the commission signing the act may be: accountant, chief accountant, cashier, etc.

The second copy of the document or its copy is sent to the employee in relation to whom the error occurred. An official letter of notification about the need to repay the overpaid amount within a certain period is attached to the act.

If the employee does not object, then, based on his application, the amount is paid in cash or by non-cash deduction from wages on other terms agreed with the administration. Often such repayment occurs in installments. According to Art. 138 of the Labor Code of the Russian Federation, as a general rule, deduction is possible in the amount of no more than 20% of each salary. It should be taken into account that the employee, in addition to the specified amount to be repaid, may have other deductions.

If an employee agrees in writing to repay the debt in cash at the cash desk or voluntarily deposit it into the company’s account, but this period has expired and the debt has not been repaid, then within the next month the manager issues an order to deduct the amount of the debt from the employee’s salary. If the employee ignores the notice or refuses to repay the overpayment, the employer may go to court.

The issue with an employee who, upon dismissal, received more than what was required by law, is resolved in the same manner as indicated above. It is advisable to immediately indicate in the notice the possibility of going to court if the debt is not repaid. Dismissed employees in most cases refuse to voluntarily repay overpayments.

Accountant's responsibility

An accountant may be held financially liable under the law if it was not possible to repay the overpayment at the expense of the employee. The basis for holding the accountant accountable can be an act recording (Labor Code of the Russian Federation, Article 247):

- the amount of material damage;

- the reason for the loss.

The amount of loss can be repaid by an accountant in two ways:

- if there is a liability agreement with him, repayment occurs in full;

- if there is no contract of liability, repayment occurs in the amount of average monthly labor payments (Labor Code of the Russian Federation, Articles 244, 248).

If the accountant does not agree to repay the amount of the error voluntarily or the month period discussed above has expired, the issue of collection is decided exclusively by the court.

On a note! The full financial responsibility of an accountant can be fixed in an employment contract with him.

Postings

If you discover an overcharged and overpaid amount, you should remember that part of this amount is income tax. Thus, the excess payment is “split” into two independent amounts and reflected in different entries.

First, the overpayment as a whole is reversed, using the same transactions by which it was accrued:

Dt20, 23, 26 Kt70 – reversal by the amount of the overpayment (payments to the Funds for overpayment are similarly reversed).

Then the personal income tax is reversed: Dt70 Kt68/NDFL – reversal of the overpayment amount (13%).

The remaining amount overpaid to the employee is reflected in account 73 with the opening of the corresponding sub-account: Dt 73 Kt 70.

The employee voluntarily pays off the debt by depositing funds into the cash register or by deducting from the salary. It is also possible to deposit funds into the company's bank account: Dt50,51,70 Kt73.

If for some reason the debt cannot be collected, then the following entries are made:

- Dt76 Kt 73;

- Dt 91/2 Kt 76.

Results

- Excess accruals and wage payments can be returned to the organization without any problems only with the written consent of the employee in respect of whom the overpayment was made, and only if the one-month period is observed after the one set for the employee to voluntarily repay.

- In other cases, the return may be contested, including in court, despite the legally established possibility of debt repayment. A detected error in payments must be recorded in an act signed by the organization’s internal commission. The employee must be familiarized with the act.

- An accountant who makes a mistake bears financial responsibility for it in accordance with the law.

- Correspondence accounts used to account for overpayments of wages are reversal entries of previously made entries. The excess amount paid in hand is reflected in Dt 73 account. Its repayment by the employee is reflected in the Dt of the corresponding accounts, depending on the method of repayment. If the loss cannot be recovered, it is transferred to Dt 76 and then recorded according to Dt 91/2.